FarFetch, Matches, What went wrong

FarFetch, Matches, What went wrong

Welcome to The Dandelion Tiger.

The Business of Shopping is a mini essay series on the future of luxury retail and shopping. I explore all the questions that keep me up at night (no lie) about where we are at in the world of commerce and consumer culture.

What right do I have to speak on the topic? Well, I like to shop: I am the perfect consumer. I consult the UK’s leading retail businesses for a living: hopefully that means I know what I am talking about.

01 explores where FarFetch & Matches went wrong, in the lead up to their respective acquisition and closure

02 (coming soon) explores where Mytheresa went right, as the sole luxury e-tailer that consistently reports a profit, and what we can learn from that

03 04 0X 0X are a work in progress

01 FarFetch, Matches, What went wrong?

The question has plagued me since it came out in December last year that FarFetch was being sold in a hurried deal to Korean e-commerce giant Coupang, leaving YNAP’s Net-a-Porter hanging by a thread once again without prospect of a buyer; this followed closely by news of Matches Fashion’s disgraceful administration.

It seemed like a sign of the times: a reflection of the state of our global economy and the challenging landscape of luxury e-commerce, after circa five years of one crisis after another. Starting with covid, compounded by geopolitical tensions between China, Russia, Ukraine, America, these stresses put all our industries to the test.

In the world of luxury multi-brand retailing, it now seems, these events have exposed a business model that maybe wasn’t all that great in the first place?

Where did it all go wrong, though, and in such a short time?

Because as recently as 2021, FarFetch was at the height of its glory. Hailed as the trailblazing, industry-disrupting, tech-forward brainchild of founder Jose Neves, everyone was placing their bets on them to emerge as a clear winner in the race for luxury’s online shopper.

Similarly, in 2017, it seemed that Tom & Ruth Chapman (founders of Matches Fashion), had reached the pinnacle of business success, living every Silicon Valley founder’s wet-dream: Matches, which began life as a humble store in London’s Wimbledon, had been sold to Apax Partners for a whopping USD 1,000,000,000 (that’s a billion, ya’ll); and after a fierce bidding war, no less.

Amidst all the noise, shock, and horror (haha) at the FarFetch and Matches news, one more silly little question slowly began to peep its little head up at me: if there was once a race for luxury’s online shopper, then a true winner has already emerged. Quiet, unassuming Mytheresa was still standing strong. Focused, in her lane, stable, profitable. How?!

Okay, SO. We will start off by looking at where FarFetch & Matches went wrong. In 02 (coming soon), we will explore where Mytheresa went right, and what we can take away from it all, in the context of the future of luxury.

The story

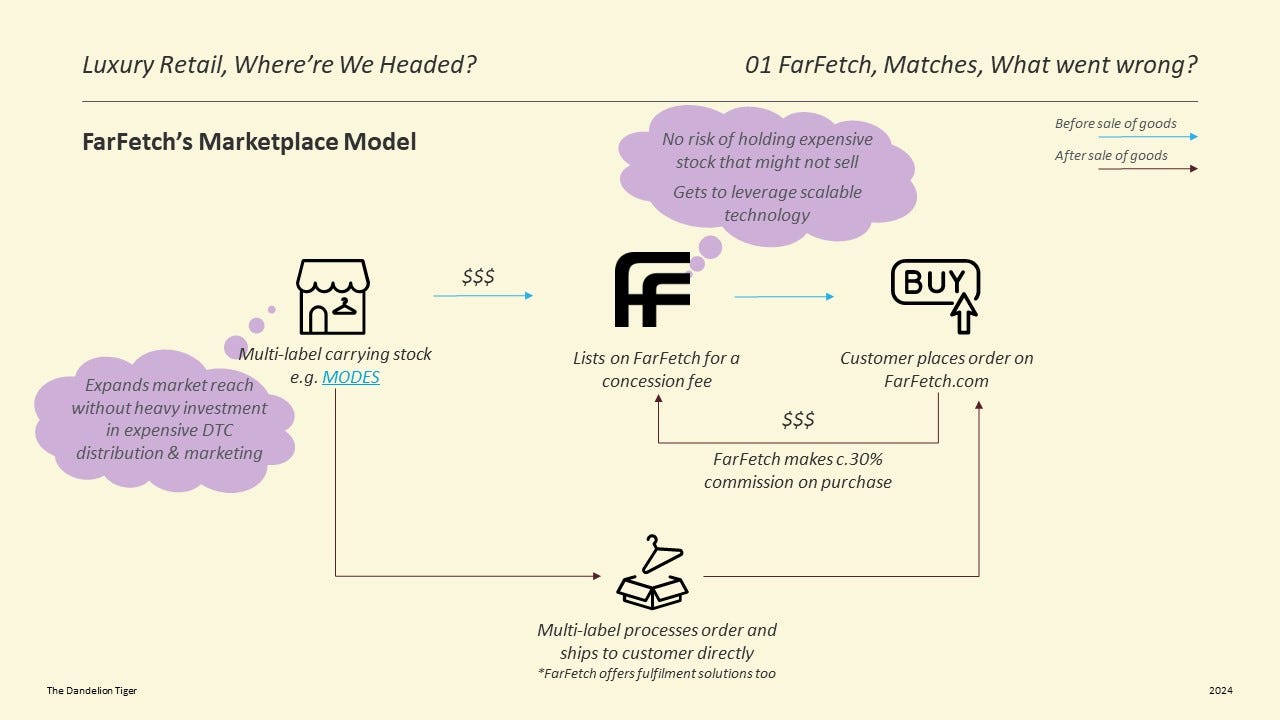

Unlike most retailers, FarFetch’s business swelled during the Covid-19 pandemic. Revenue increased 64% year-on-year between 2019 and 2020, up to USD 1.7 billion, in part thanks to the nearly 900,000 new customers shopping on its platform.

At a time when competitors’ supply chains were blocked up by warehouse closures and closed borders, FarFetch’s no-stock marketplace model flourished.

For comparison, traditional e-tailors like Net-a-Porter & Matches buy and hold stock from brands, which means higher costs of storing the goods, exposure to fleeting seasonal trends leading to margin-cutting discounts, and reliance on a linear supply network.

Net-a-Porter, for example, had to pause operations at the height of covid restrictions, because its UK warehouses had to shut. FarFetch avoided blockers of this type thanks to its diverse supply network of boutiques and fulfilment centres worldwide.

The perils of riding a wave

As the tidal wave of post-pandemic shopping abundance began to recede, from Q2 2021, the cracks in FarFetch’s operations started to emerge. See below graphic showing its stock price over the past 5 years; spiking at the height of covid-related lockdowns in 2020 and beginning to dive from early 2021.

Riding the Covid wave, FarFetch had doubled down on its ambitions.

It took on additional $1.5bn in funding to start a Chinese-based joint venture. It went on a hiring spree in 2021, continued to make acquisitions and investing in deals with other retailers (i.e. $200million investment into a Neiman Marcus deal).

Right around here is when things started to go downhill.

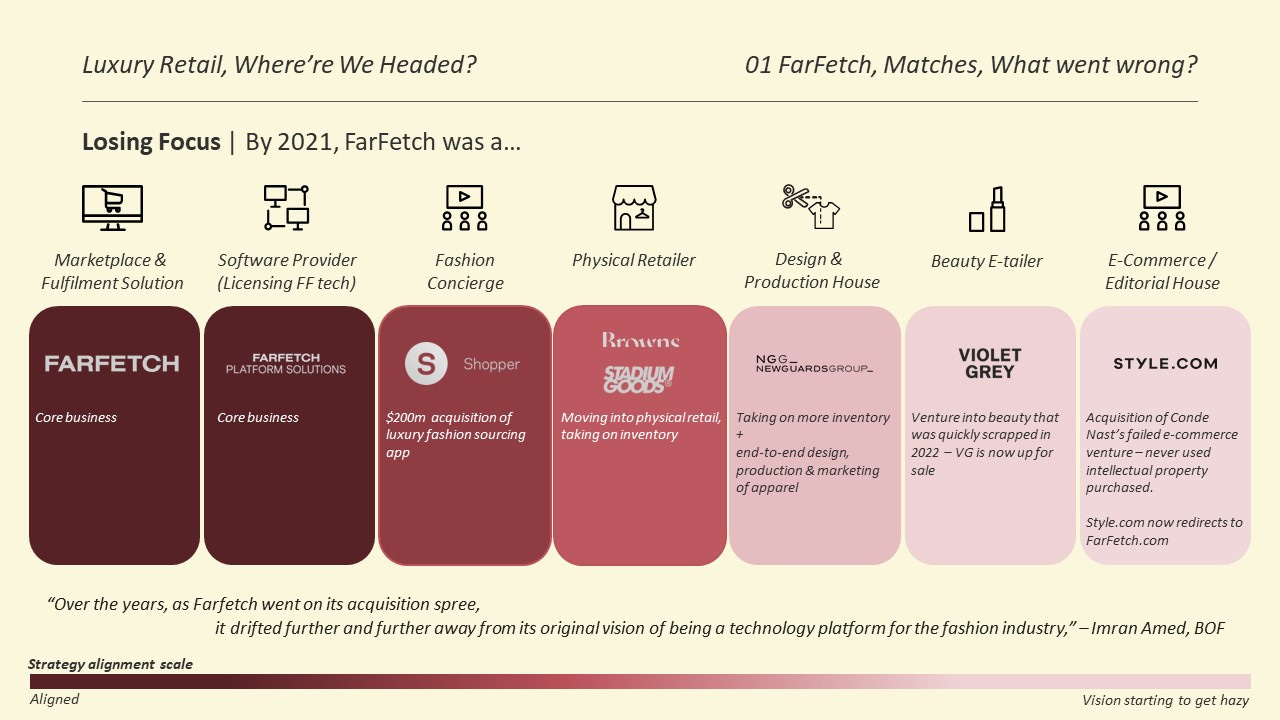

Losing Focus

By 2021, FarFetch was doing a lot.

It was burning through cash much more quickly than it was bringing in (see ‘Fashion Concierge’ box in above slide. FF purchased a fashion-sourcing app started by Neve’s wife Daniela Cecilio for $200m. Note this number, compared to the c.$70m that Matches eventually sold to Frases group for).

All the while, voting and decision-making rights remained largely with Neves, meaning that FarFetch was at times slow to react to market changes.

The cash burn caught up: FarFetch had $1.6bn debt repayments due between 2027 and 2030, and investors lost hope that the business would be able to cover their liabilities. At the end of 2023, credit rating agency Moody’s downgraded FF stock to Caa2, ‘deep junk territory’, according to the Financial Times.

Its sale to Coupang was announced shortly after, a last-minute deal that narrowly saved it from the same fate that Matches met.

Instability, confusion at Matches

Amongst other factors that eventually led to its administration, Matches faced similar problems with aligning to a single vision. News of its shuttering came as no surprise to certain industry insiders in the know -

"I saw this coming. Apax has short-term objectives. When the original owners, Tom and Ruth, owned the business, they knew their customers. They curated an aspirational offer that complemented the customer journey. They had a clear vision and ambience around the Matches brand. Unlike Apax, who sent mixed messages to their audience."

Pan Philippou, a well-known fashion consultant and investor, in interview with TheIndustry.fashion

Things started to go downhill for Matches quickly after its first acquisition by Apax. The general sentiment is that Apax realised they had overpaid for the business; and when you’ve already overpaid for something, you’re not as willing to invest even more money into it. Here’s the problem in that though: In such a competitive landscape, where margins are tight and competition is fierce, businesses need continuous investment and commitment to stay healthy.

Over the years since its acquisition by Apax and later by Frasers, Matches saw many a turnaround plan proposed by business leadership, including rebranding from Matchesfashion to Matches. It seems, however, that these plans were never given a chance to be properly implemented, and eventually all failed.

Instability was a problem too: between 2019 – 2023, Matches had seen 4 different CEOs. After Ulric Jerome, who served for six years, all the business’ successive CEOs served for no more than one year each.

With each change in leadership and parent-group, the business lost more and more of what made it so beloved in the first place: tight curation that spoke to its customers.

Instability and lack of commitment seems to be the final straw that broke the camel’s back at Matches, with Frasers citing that too much investment was needed to turn the company around.

Note: not impossible, just not willing to commit.

So the final picture is this:

FarFetch and Matches both had very promising beginnings. FarFetch’s technology and marketplace model gave it a strong edge over its competition; and Matches had a deep heritage working for it amongst the London fashion set.

In the end, FarFetch maybe flew too close to the sun - took on too much funding and put it in too many baskets; while Matches seemed not to have enough conviction from its owners, who were unwilling to give it a fair chance.

All in all I still believe FarFetch and Matches have strong business propositions that bring true value to their customers. It is a shame that along the way, both businesses began to lose focus of what made them great in the first place, had trouble with investment, and faced countless disruptions well beyond their control.

Reflecting now on this essay, I empathise most with Jose Neves and his team, who built FarFetch from the ground up and stuck with it through the 2008 financial crisis and aftermath to now. His proposition pre-IPO was a strong one; FarFetch never had any trouble getting large sums of funding because of it, and this essay from one of their earliest investors illustrates why: The Farfetch journey, 10 years from start-up to IPO. It is sad to see that the years of work has resulted in FarFetch instead becoming a cautionary tale: but I suppose the story isn’t over. FarFetch is still operating. And we don’t know yet what will happen to Matches (there are whispers of Frasers buying it back, as it did with USC). So, we’ll keep watching this space.

If you are as curious as I am about how and why Mytheresa is still doing it all right, or at least seems to be, 02 of Luxury Retail, Where’re We Headed? is coming in the next week or so. Subscribe to follow along.

Notes

Sharing some notes on other factors affecting FarFetch, Matches and the luxury e-commerce business as a whole. I decided not to go into them in detail in this first segment, but these points are nonetheless relevant and may be discussed in later parts of the series.

Recommended reading: The Farfetch journey, 10 years from start-up to IPO.

Economic & Geopolitical Impact

On top of all that, FarFetch was, according to its latest available financial report (year-ended 2022) and other sources, now:

Struggling with a decreased appetite from Chinese shoppers, as China struggled to recover from the impacts of Covid

Struggling with lower demand from the Middle East & Europe due geopolitical conflict

Seeing aspirational shoppers’ purse strings tighten due to rising inflation

Seeing costs rise due to inflation

Problems with luxury e-tailing

Big players are unwilling to list on platforms like FarFetch & Matches, preferring to maintain branding and exclusivity by keeping control of their distribution

Low negotiating power: margins are tight because luxury retailers need big brands more than the big brands need them

High customer acquisition costs and strong competition

So interesting, thanks for sharing your analysis ! As a marketplace startup founder, I was so inspired by Farfetch tech model and the fact it was also empowering local luxury boutiques, beyond brands. Too bad it didn’t last.

This is so fascinating!